Which is the most tax-efficient canton for companies in 2025?

Swiss companies pay varying corporate tax rates depending on their canton of residence. These include profit tax on earnings and capital tax on equity. These taxes are levied at federal, cantonal, and municipal levels. As a result, there is significant tax competition between the country’s 26 cantons, with profit tax rates in cantonal capitals ranging from 11.85% to 20.54% in 2025.

In this article, we examine the most tax-efficient Swiss cantons for businesses in 2025, compare profit and capital tax rates across all regions, and explain how strategic location choice can substantially reduce your company’s overall tax burden.

Book a free initial consultation with our experts.

Book a callHighlights

- Zug, Lucerne, and Nidwalden offer the lowest corporate taxes in 2025 (under 12%)

- Profit tax rates range from 11.85% (Zug) to 20.54% (Bern) across Switzerland’s cantonal capitals

- Central Switzerland dominates the low-tax rankings with highly competitive rates

- Strategic canton selection can save businesses up to 8.7 percentage points in taxes

- Capital tax rates must be considered alongside profit tax for optimal location choice

Content

- Which is the most tax-efficient canton for companies in 2025?

- Highlights & content

- What are the different types of corporate taxation in Switzerland and who do they apply to?

- How do the taxation of partnerships and corporations differ?

- How is profit tax calculated for corporations?

- What are the current capital and profit tax rates across Swiss cantons?

- Which cantons are the most and least tax-friendly for corporations?

- How have canton tax rates responded to global minimum tax and economic pressures?

- The importance of capital tax in total tax burden

- Get expert tax advisory support from Nexova

- FAQ

- Trusted by over 150 companies

What are the different types of corporate taxation in Switzerland and who do they apply to?

The term “corporate taxes” refers to the entire range of taxes payable by corporations such as GmbHs and AGs. The primary corporate taxes are profit tax (on earnings) and capital tax (on equity).

In addition to these primary corporate taxes, businesses may also be subject to church tax (mandatory in most cantons), withholding tax on dividends, and value-added tax (VAT) for companies with annual turnover exceeding CHF 100,000.

Partnerships and sole proprietorships are not subject to corporate tax. Instead, business owners pay personal income tax and wealth tax on their business earnings and assets (the same taxes that apply to individuals).

In principle, all corporations domiciled in or managed from Switzerland must pay corporate taxes, while partnerships and sole proprietorships are taxed through their owners’ personal tax returns.

New to Swiss corporate taxation? Check out our comprehensive tax crash course for founders, which covers everything from filing deadlines to social security obligations.

Book a free initial consultation with our experts.

Book a callHow do the taxation of partnerships and corporations differ?

The key difference in the taxation of partnerships versus corporations lies in legal entity status: partnerships and sole proprietorships are taxed through their owners’ personal income and wealth tax, while corporations are taxed as separate legal entities with corporate profit and capital taxes.

This creates a potential double taxation for corporations, as both the company and its shareholders pay tax, whereas partnerships only face single-level taxation at the owner level.

For a complete comparison of legal forms in Switzerland, including sole proprietorships, GmbHs, AGs, and partnerships, see our detailed analysis of how each structure affects your tax obligations.

Partnerships: taxes on private and business assets

Partnerships, such as limited partnerships, general partnerships and sole proprietorships, are not considered legal entities in Switzerland. Therefore, they are not subject to corporate tax in the traditional sense.

Instead, sole proprietors and partners pay taxes on all their assets and income, both private and business, to the federal, cantonal and municipal authorities. These are all viewed as personal taxes. Unlike corporations (which can deduct tax expenses when calculating their taxable profit), partnerships and sole proprietorships cannot deduct the personal taxes they pay from their business income.

Corporations: separation of business and private assets

There is a clear separation between business and private assets in corporations such as GmbHs and AGs. The company itself is taxed, while shareholders and partners pay income taxes on dividends and pay wealth taxes according to the share value.

This arrangement leads to a double tax burden, as both the company, and the partners or shareholders, pay taxes.

Book a free initial consultation with our experts.

Book a callHow is profit tax calculated for corporations?

Fundamentals of the profit tax calculation

Profit tax, also known as income tax, is levied on corporations such as GmbHs and AGs on the basis of their taxable profit. The Confederation levies a fixed tax rate of 8.5% (as at the time of writing) on the profit after tax (equivalent to approximately 7.8% on pre-tax profit).

Cantons and municipalities levy their own profit taxes on top of the federal rate, with rates varying significantly across Switzerland. This variation creates the wide range of combined tax rates shown in the cantonal comparison below.

Church taxes for companies

Most cantons also levy church taxes in addition to profit tax. These taxes benefit the Reformed, Roman Catholic, Christian Catholic churches or the Jewish community. Church tax is mandatory for companies in these cantons and, unlike private individuals, they cannot leave the church to avoid this tax liability.

Book a free initial consultation with our experts.

Book a callWhat are the current capital and profit tax rates across Swiss cantons?

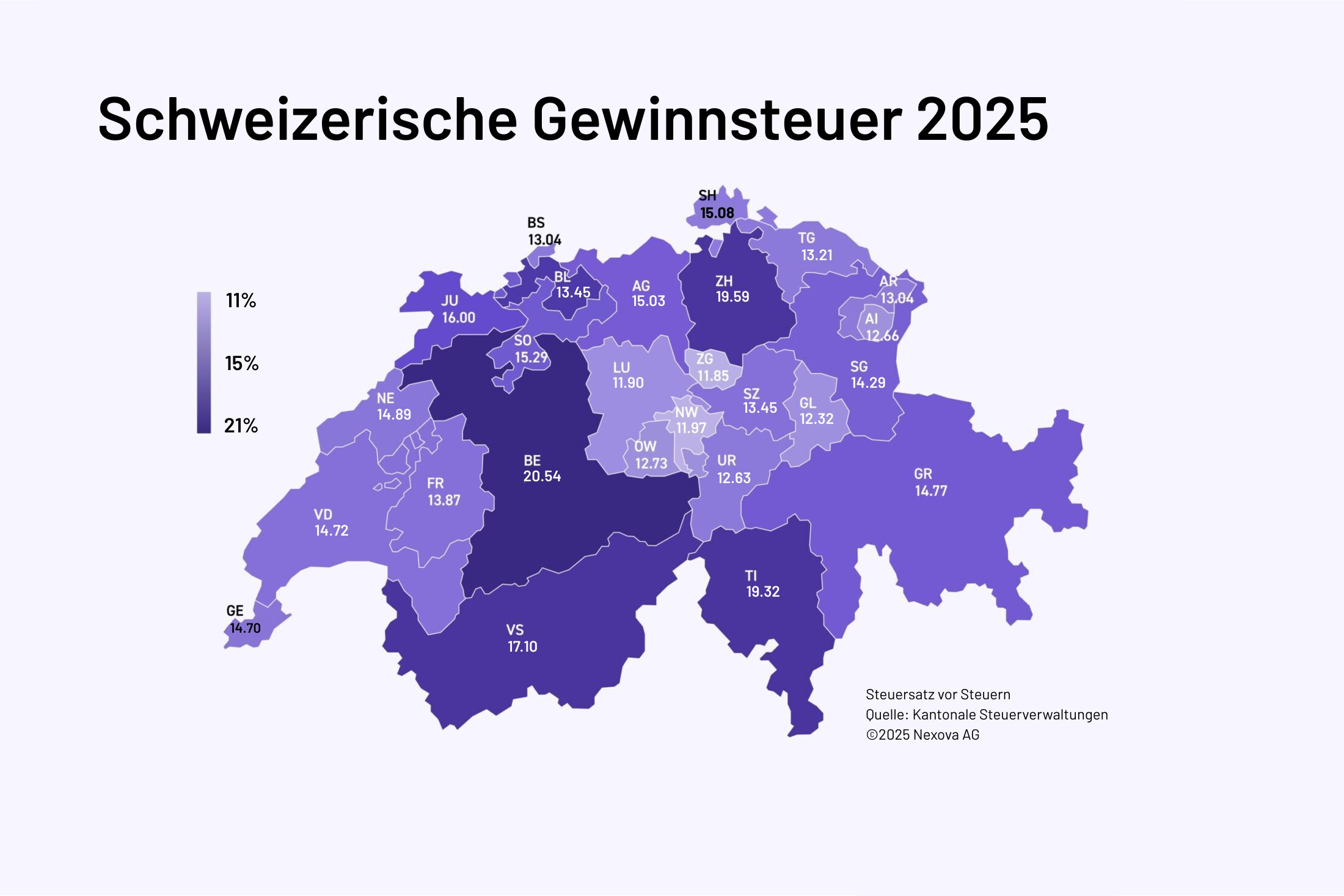

The average corporate tax rate in Switzerland is 14.4% in 2025, down from 14.6% in the previous year. The canton of Zug remains the most tax-friendly canton overall with a profit tax rate of 11.85% in the capital, while Canton Bern has the highest maximum rate at 20.54% (though it applies a progressive structure starting from 13.17%).

Here is a summary of the profit tax rates (on profit before tax) applied in the capital municipality/city of each of the 26 cantons in ascending order. In cantons which apply a progressive profit tax structure, the highest progressive rate is given here:

Profit tax rates across Switzerland’s 26 cantons

- Zug (ZG): 11.85%

- Lucerne (LU): 11.90%

- Nidwalden (NW): 11.97%

- Glarus (GL): 12.32%

- Uri (UR): 12.63%

- Appenzell Innerhoden (AI): 12.66%

- Obwalden (OW): 12.73%

- Basel-City (BS): 13.04%

- Appenzell Ausserrhoden (AR): 13.04%

- Thurgau (TG): 13.21%

- Basel-Landschaft (BL): 13.45%

- Schwyz (SZ): 13.45%

- Fribourg (FR): 13.87%

- St. Gallen (SG): 14.29%

- Geneva (GE): 14.70%

- Vaud (VD): 14.72%

- Graubünden (GR): 14.77%

- Neuchâtel (NE): 14.89%

- Aargau (AG): 15.03%

- Schaffhausen (SH): 15.08%

- Solothurn (SO): 15.29%

- Jura (JU): 16.00%

- Valais (VS): 17.10%

- Ticino (TI): 19.32%

- Zurich (ZH): 19.59%

- Berne (BE): 20.54%

{kind=link}

Below is a more detailed overview of the profit and capital tax rates across each canton for 2025. Please note:

- All tax rates shown are effective rates on profit before tax.

- For progressive cantons, the first rate shown is the lowest marginal rate and the second rate represents the maximum marginal rate that applies at higher profit levels.

- In each case, the tax rates are provided for the cantonal capital and for the most tax-friendly municipality.

- Where minimum taxes are listed with a slash (e.g., CHF 361 / CHF 247), the first figure refers to the capital municipality and the second to the lowest-tax municipality.

All rates listed below have been independently tested and verified by Nexova’s tax experts using the official Swiss tax calculator.

Profit and capital tax rates across Switzerland’s 26 cantons (including most tax-friendly municipality in each canton)

Canton Zug

- Municipality of Baar: profit tax: 11.82%, capital tax: 0.07%

- City of Zug: profit tax: 11.85%, capital tax: 0.07%

- Minimum tax: CHF 353 / CHF 351

Canton of Lucerne

- Municipality of Lucerne: profit tax: 11.90%, capital tax: 0.08%

- Municipality of Meggen: Profit tax: 11.09% (lowest in Switzerland), capital tax: 0.07%

- Minimum tax: CHF 500

Canton Nidwalden

- Municipality of Stans: profit tax: 11.97%, capital tax: 0.01%

- Uniform rate across all communes

- Minimum tax: CHF 500

Canton Glarus

- Municipality of Glarus: profit tax: 12.32%, capital tax: 0.25%

- Glarus is both the capital and the lowest-tax municipality

Canton Uri

- Municipality of Altdorf: profit tax: 12.63%, capital tax: 0.001%

- Municipality of Seedorf: profit tax: 12.59%, capital tax: 0.001%

- Minimum tax: CHF 500

Canton of Appenzell Innerhoden

- Municipality of Appenzell: profit tax 12.66%, capital tax: 0.05%

- Uniform tax rate for all communes

- Minimum tax: CHF 500

Canton Obwalden

- Municipality of Sarnen: profit tax: 12.73%, capital tax: 0.001%

- Uniform rate across all communes

- Minimum tax: CHF 500

Canton Basel-Stadt

- City of Basel: profit tax: 13.04%, capital tax: 0.10%

- Municipality of Bettingen: profit tax: 12.42%, capital tax: 0.09%

- No minimum tax

Canton Appenzell Ausserrhoden

- Municipality of Herisau: profit tax: 13.04%, capital tax: 0.05%

- Uniform rate across all municipalities

- Minimum capital tax: CHF 876

Canton Thurgau

- Municipality of Frauenfeld: profit tax: 13.21%, capital tax: 0.04%

- Municipality of Bottighofen: Profit tax: 12.19%, capital tax: 0.03%

- Minimum capital tax: CHF 538 / CHF 430

Canton Schwyz

- Municipality of Schwyz: profit tax: 13.45%, capital tax: 0.01%

- Municipality of Wollerau: profit tax: 11.75%, capital tax: 0.01%

- Minimum capital tax: CHF 361 / CHF 247

Canton Basel-Landschaft

- Municipality of Liestal: profit tax: 13.45%, capital tax: 0.16%

- Municipality of Giebenach: profit tax: 12.55%, capital tax: 0.15%

- Minimum capital tax: CHF 480

Canton of Fribourg

- City of Fribourg: profit tax: 13.87%, capital tax: 0.19%

- Commune of Greng: profit tax: 12.40%, capital tax: 0.14%

- No minimum tax

Canton St.Gallen

- City of St.Gallen: Profit tax: 14.29%, capital tax: 0.06%

- Uniform rate across all municipalities

- Minimum tax: CHF 292

Canton of Geneva

- City of Geneva: Profit tax: 14.70%, capital tax: 0.40%

- Municipalities of Genthod and Cologny: profit tax: 14.30%, capital tax: 0.37%

- No minimum tax

Canton of Vaud

- City of Lausanne: profit tax: 14% / 14.72% (progressive), capital tax: 0.14%

- Municipality of Eclépens: profit tax: 13.19% / 13.82% (progressive), capital tax: 0.12%

- Progressive structure: The higher rate (14.72% for Lausanne, 13.82% for Eclépens) applies to profits exceeding CHF 10 million (i.e., only affects larger corporations)

Canton Graubünden

- City of Chur: profit tax: 14.77%, capital tax: 0.46%

- Uniform rate across all municipalities

- Minimum tax: CHF 200

Canton Neuchâtel

- City of Neuchâtel: profit tax: 13.57% / 14.89% (progressive), capital tax: 0.50%

- Uniform rate across all communes

- Progressive tax starts increasing after approximately CHF 5 million profit (i.e., only affects larger corporations)

- No minimum tax

Canton Aargau

- City of Aarau: Profit tax: 15.03%, capital tax: 0.13%

- Uniform rate across all municipalities

- Minimum tax: CHF 835

Canton Schaffhausen

- Municipality of Schaffhausen: profit tax: 12.02% / 15.08% (progressive), capital tax: 0.001%

- Municipality of Buchberg: profit tax: 11.04% / 13.44% (progressive), capital tax: 0.001%

- Progressive structure: Schaffhausen uses a two-tier system. Companies pay the lower rate (12.02% for Schaffhausen or 11.04% for Buchberg) on profits up to CHF 5 million. Above CHF 15 million, the rate reaches its maximum (15.08% or 13.44% respectively).*

- Minimum tax: CHF 191 / CHF 145

Canton Solothurn

- City of Solothurn: profit tax 15.29%, capital tax: 0.17%

- Municipality of Kammersrohr: Profit tax: 13.94%, capital tax: 0.14%

- Minimum capital tax: CHF 434 / CHF 350

Canton Jura

- City of Delémont: profit tax: 16.00%, capital tax: 0.19%

- Municipality of Les Breuleux: profit tax: 15.09%, capital tax: 0.16%

- No minimum tax

Canton Valais

- City of Sion: profit tax: 11.96% / 17.12% (progressive), capital tax: 0.49%

- Uniform rate across all communes

- Progressive structure: 11.96% on first CHF 250,000 profit, then 17.12%

- Minimum capital tax: CHF 200

Canton Ticino

- City of Bellinzona: profit tax: 19.32%, capital tax: 0.29%

- Municipality of Porza: profit tax: 17.34%, capital tax: 0.23%

- No minimum tax

Canton of Zurich

- City of Zurich: profit tax: 19.59%, capital tax: 0.17%

- Municipality of Kilchberg: profit tax: 17.28%, capital tax: 0.13%

- No minimum tax

Canton of Bern

- City of Bern: profit tax: 13.17% / 20.54% (progressive), capital tax: 0.02%

- Municipality of Deisswil b. Münchenbuchsee: profit tax: 12.43% / 18.88% (progressive), capital tax: 0.02%

- Progressive structure: base rate of 13.17% (Bern) or 12.43% (Deisswil) increases steadily above CHF 10,000 profit

- No minimum tax

The following additional details should be noted about progressive and special rate structures:

- Canton Bern applies a progressive structure starting at 13.17%, increasing steadily above about CHF 10,000 profit until reaching its maximum rate of 20.54%

- Canton Valais levies 11.96% on the first CHF 250,000 of profit, then 17.12% on all profit thereafter

- Canton Vaud applies the higher rate (14.72% for Lausanne) on profits exceeding CHF 10 million

- Canton Neuchâtel has progressive rates starting to increase after approximately CHF 5 million profit

- Canton Schaffhausen uses a two-tier system: lower rates apply up to CHF 5 million profit, reaching maximum rates above CHF 15 million

* Technical note on Schaffhausen’s structure: The first rate applies up to CHF 5 million profit (after tax). Between CHF 5-15 million, a much higher marginal rate applies, bringing the overall effective rate up to the maximum level (15.08% for Schaffhausen, 13.44% for Buchberg). From CHF 15 million (after tax) onwards, the rate stabilizes at this maximum effective level.

Book a free initial consultation with our experts.

Book a callWhich cantons are the most and least tax-friendly for corporations?

Central Switzerland clearly dominates the low-tax rankings, with Zug (11.85%), Lucerne (11.90%), and Nidwalden (11.97%) offering the most competitive rates. On the opposite end, Canton Bern has the highest maximum rate at 20.54%, though this only applies to larger profits due to its progressive structure. Zurich follows at 19.59% and Ticino at 19.32%.

The difference between Switzerland’s lowest and highest cantonal capital rates spans 8.69 percentage points (from Zug at 11.85% to Bern at 20.54%) representing substantial long-term savings potential for businesses.

At the municipal level, Meggen in Canton Lucerne offers the absolute lowest profit tax rate in Switzerland at 11.09%, followed by Wollerau (Schwyz) at 11.75% and Baar (Zug) at 11.82%.

Several cantons occupy the middle ground with rates around the Swiss average of 14.4%, including St. Gallen (14.29%), Geneva (14.70%), and Vaud (14.72%). These cantons often offset moderate tax rates with other advantages such as strategic location, access to top talent, or industry clusters.

Book a free initial consultation with our experts.

Book a callHow have canton tax rates responded to global minimum tax and economic pressures?

The implementation of the OECD’s global minimum tax of 15% for large multinational enterprises (consolidated revenues exceeding EUR 750 million in at least two out of the last four years) has prompted varied strategic responses across Swiss cantons.

Several jurisdictions adjusted their rates in 2024-2025 to optimize their position within the new framework. While some cantons raised their tax rates in connection with the global minimum tax (particularly for large, highly profitable corporations through new progressive tax structures), other cantons completed reductions initiated under earlier tax reforms.

Basel-Landschaft made the most significant reduction, cutting its corporate tax rate by 2.45 percentage points to 13.45%. This lower rate primarily benefits the 99% of Swiss companies that fall below the EUR 750 million threshold and remain unaffected by international minimum tax requirements.

Other cantons have taken different approaches, strategically raising rates on large corporations to capture revenue that may otherwise be collected as top-up taxes by other jurisdictions.

Geneva increased its standard rate in 2024 already from 14% to 14.7% across the board. Vaud and Neuchâtel introduced progressive structures, with Vaud applying a higher 14.72% rate to companies with profits exceeding CHF 10 million, and Neuchâtel increasing rates after about CHF 5 million profit to finally reach an effective tax rate of 14.89% at the extremely high profit levels (hundreds of millions of Swiss franc). This approach ensures they collect tax from large MNEs that fall under global minimum tax rules while preserving competitive rates for SMEs.

The canton of Schaffhausen implemented a unique progressive structure in 2024, where profits exceeding CHF 15 million face an effective rate of 15.08% to align with global minimum tax requirements, while smaller companies with profit after tax of less than CHF 5 million continue benefiting from the lower 12.02% base rate.

Finally, the canton of Basel-Stadt looks set to follow suit by increasing its tax rate from 13.04% to 14.53% on profits in excess of CHF 50 million from 2026 onward.

The overall Swiss corporate tax average declined from 14.6% to 14.4% in 2025, demonstrating that competitive pressure among cantons continues despite international harmonization efforts.

Book a free initial consultation with our experts.

Book a callThe importance of capital tax in total tax burden

While profit tax rates receive the most attention, capital tax can significantly impact your total tax burden and should be a key factor in canton selection. Capital tax is levied on a company’s equity (share capital plus reserves) and varies considerably across cantons, with some charging as much as 0.5% while others levy minimal or no capital tax.

Example: Comparing Total Tax Burden

Consider two companies, each with CHF 1 million in annual profit but CHF 10 million in equity capital:

Company A in Neuchâtel (lower profit tax):

- Profit tax: CHF 1,000,000 × 13.57% = CHF 135,700

- Capital tax: CHF 10,000,000 × 0.50% = CHF 50,000

- Total tax burden: CHF 185,700

Company B in St. Gallen (higher profit tax):

- Profit tax: CHF 1,000,000 × 14.29% = CHF 142,900

- Capital tax: CHF 10,000,000 × 0.06% = CHF 6,000

- Total tax burden: CHF 148,900

Despite St. Gallen having a profit tax rate 0.72 percentage points higher than Neuchâtel (14.29% vs 13.57%), Company B pays CHF 36,800 less annually due to the substantial difference in capital tax rates (0.06% vs 0.50%).

This example illustrates why comparing profit tax rates alone can be misleading. Particularly for companies with significant equity capital (such as holding companies, capital-intensive businesses, or companies in growth phases), the total tax burden should guide canton selection rather than profit tax rates in isolation.

In some cases, a canton with a slightly higher profit tax but minimal capital tax may prove more advantageous than a low-profit-tax jurisdiction with substantial capital taxes.

Book a free initial consultation with our experts.

Book a callGet expert tax advisory support from Nexova

Choosing the right canton for your business involves weighing multiple factors beyond tax rates alone, including regulatory requirements, administrative processes, and whether the location aligns with your company’s long-term goals. Nexova’s tax advisors can help you evaluate these considerations and understand the full tax implications of different location choices.

Whether you’re establishing a new company in Switzerland or considering relocation, our team provides practical guidance on corporate tax planning and compliance requirements. Contact Nexova today to discuss your specific situation.

FAQ

Answers at a click

Which is the most tax-friendly Swiss canton?

Zug is widely considered Switzerland’s most tax-friendly canton overall, combining a very low profit tax rate of 11.85% for the capital city with a minimal capital tax of 0.07%.

Lucerne and Nidwalden offer similarly competitive tax levels, with Lucerne at 11.90% and Nidwalden at 11.97%. At the municipal level, Meggen in Canton Lucerne offers the absolute lowest profit tax rate in Switzerland at 11.09%.

How do Swiss corporate tax rates compare internationally?

Switzerland remains highly competitive globally. Even the highest Swiss rates (around 20%) are moderate compared to most developed economies.

The Swiss average of 14.4% compares favorably to neighboring countries like France (25%), Germany (~30%), and Italy (~24%), making Switzerland an attractive jurisdiction for international businesses.

How much can businesses save by choosing the right canton?

Among cantonal capitals, the difference between the lowest-tax location (Zug at 11.85%) and highest-tax location (Bern at 20.54%) is 8.69 percentage points, representing substantial long-term savings for profitable companies.

At the municipal level, the range extends even further, with Meggen offering rates as low as 11.09% compared to the 22.3% highest progressive profit tax rate found in the municipality of Schelten in Canton Bern.

Do minimum taxes significantly impact small businesses?

Yes, many cantons impose minimum taxes regardless of profitability. For example, Appenzell Ausserrhoden requires CHF 876 annually in capital tax, Aargau requires CHF 835, and several cantons require CHF 500 minimum overall tax. These can burden small startups with limited profits.

For a complete breakdown of minimum tax requirements by canton, including five-year exemptions available in some locations, see our dedicated analysis.

What changes occurred in Swiss corporate tax rates during 2025?

Several cantons made significant adjustments to their corporate tax rates in 2024 and 2025, with Basel-Landschaft reducing its rate by 2.45 percentage points to 13.45%.

The overall Swiss average decreased from 14.6% to 14.4%, reflecting continued competitive pressure among cantons.

Which cantons use progressive tax structures?

Several cantons apply progressive rates that increase as profits grow:

– Bern: 13.17%-20.54% (increases steadily above CHF 10,000 profit)

– Valais: 11.96%-17.1% (higher rate kicks in above CHF 250,000)

– Vaud: 13.92%-14.72% (higher rate applies above CHF 10 million)

– Neuchâtel: 13.57%-14.89% (increases after CHF 5 million, with the highest rate only reached at extremely high profit levels)

– Schaffhausen: 12.02%-15.08% (two-tier system: lower rate up to CHF 5 million, maximum rate above CHF 15 million)

Can I move my company to a more tax-efficient canton?

Yes, established companies can relocate to different cantons, though the process involves legal and administrative steps including updating commercial register entries, notifying tax authorities, and potentially adjusting corporate documents.

The complexity and cost should be weighed against long-term tax savings. Nexova can advise on the relocation process and whether it makes financial sense for your situation.

Trusted by over 250 companies

Discover the diversity of our customers

As an internationally active biotechnology company that stands for innovation and the highest quality, we work exclusively with partners who meet our high standards. Nexova consistently impresses us with exceptional service quality, robust processes, and an impressive pace. The professional, solution-oriented, and efficient collaboration allows us to fully focus on our core business. Additionally, we would like to highlight the remarkable cost savings of 35% compared to in-house accounting. We particularly appreciate how Nexova quickly understands, develops, and promptly implements complex requirements – both within Switzerland and at our international subsidiaries. We can wholeheartedly recommend the Nexova team.

Nexova AG offers highly professional accounting services that have significantly enhanced our financial management at Learning Lab. Their team is precise and reactive, always delivering accurate and timely reports while promptly addressing our queries. With Nexova AG’s support, we manage our clients’ accounts and finances more efficiently. We highly recommend Nexova AG for their exceptional accounting services.

For us as a new catering company, it is essential that our trustee understands our specific needs and responds flexibly to our requirements. In Nexova AG, we have found the ideal partner who supports us competently in all fiduciary matters and actively promotes our growth.

Uncomplicated or serious? Or is it and? A young, clever team is at work here, offering excellent services, highly uncomplicated and competent. Instead of a prestigious reception, expensive offices and chocolates, there are fast services and competent services. For me as a one-man company, this is exactly what I need.

Arvy AG has found an exceptional partner in Nexova AG. Their very high level of expertise in FINMA-regulated industries ensures that our financial transactions are in safe and competent hands. What sets Nexova apart is their flat-rate pricing structure, which has helped us greatly with budgeting and financial planning. As a company committed to long-term success and integrity in investments, we are very satisfied with the services provided by Nexova AG.

For us as an EdTech startup, it is very important that our trustee is as digital and agile as we are. With Nexova AG, we have found the perfect partner who can actively support us in our growth.